When we published our Q1 market update in April, investors were facing one of the most uncertain environments in recent years. Escalating conflict in the Middle East, renewed concerns over inflation and fears of higher interest rates combined to create significant volatility across global financial markets. Oil prices briefly surged to almost $120 per barrel, prompting fresh concerns that inflationary pressures could once again become embedded across developed economies.

At the time, our message was simple: Stay the Course. Resist the temptation to react to short-term market movements and remain focused on your long-term objectives.

Three months later, that advice has proven prescient. While the headlines suggested investors should panic, markets once again demonstrated why they shouldn't.

Geopolitics dominated the headlines

Much of the second quarter was overshadowed by conflict in the Middle East. As tensions escalated, investors feared disruption to global energy supplies, particularly through the strategically important Strait of Hormuz. Energy prices rose sharply and financial markets experienced periods of heightened volatility as investors attempted to assess the potential economic consequences.

Thankfully, diplomatic efforts now appear to be gaining traction and markets have responded accordingly. Oil prices have retreated significantly from their peak, inflation expectations have moderated and much of the initial market volatility has subsided.

This serves as an important reminder that financial markets are forward-looking. They respond not only to current events, but to changing expectations about what lies ahead.

| Commodity | 1-Month Change | 12-Month Change |

|---|---|---|

| Gold | +2.8% | +43.5% |

| Silver | +4.9% | +31.8% |

| Copper | +9.1% | +24.6% |

| Brent Crude Oil | -23.6% | +13.4% |

| EU Natural Gas (TTF) | -7.2% | +18.9% |

* Figures correct as at close of business 25/06/2026

Inflation and interest rates remain the key economic story

While geopolitics dominated the headlines, inflation and monetary policy continued to shape investor sentiment. In the UK, market expectations for interest rates have undergone a significant reversal over the course of the year.

At the start of 2026, investors were anticipating several Bank of England rate cuts as inflation continued to moderate and growth remained subdued. However, that narrative shifted sharply during the second quarter as inflation fears became heightened.

Currently, investors are pricing in fewer cuts through 2026 than at the start of the year. Based on overnight index swap (OIS) pricing, markets are implying between zero and one 25bp rate cuts over the course of 2026, leaving Bank Rate within the 3.50%–3.75% range for the rest of the year.

Politics close to home

Political developments have also contributed to market uncertainty. In the UK, questions surrounding the Government's leadership, fiscal position, public borrowing and future taxation have periodically unsettled gilt markets. Although these developments rarely dominate international headlines, they influence UK and IOM borrowing costs, sterling and investor confidence.

What about the "AI bubble"?

Another recurring theme throughout the quarter has been whether enthusiasm surrounding artificial intelligence has created another technology bubble. There is little doubt that valuations for some AI-related companies have become elevated. A relatively small number of technology firms continue to account for a significant proportion of global equity market returns, prompting inevitable comparisons with the dot-com era.

However, there are important differences.

At the height of the technology bubble in 2000, many companies traded on extraordinary valuations despite generating little — or no — profit. Today, many of the market leaders in AI are among the world's most profitable businesses, generating substantial cash flows and reporting robust earnings growth. While valuation metrics remain above long-term averages, they remain considerably below the extremes witnessed during the dot-com boom.

That does not mean share prices will rise indefinitely, nor that we should be surprised by periods of volatility. But many current valuations are supported by genuine earnings, significant investment and rapidly growing demand for AI infrastructure, rather than speculation alone.

Markets reward patience

Investors who reacted emotionally to geopolitical events at the start of the year risked missing the subsequent recovery as markets quickly refocused on economic fundamentals and corporate earnings. Those who remained invested were generally rewarded as sentiment improved.

This is precisely why successful investing should never be driven by today's headlines. Markets have consistently demonstrated an ability to recover from wars, political uncertainty, inflationary shocks and financial crises. While each event feels unique at the time, history repeatedly shows that remaining invested has proven more successful than attempting to predict the next market movement.

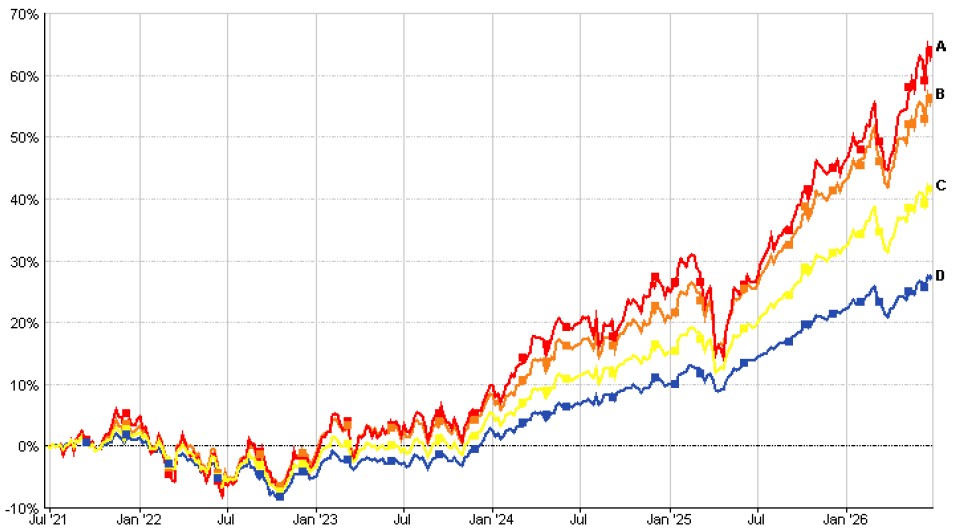

Edgewater Portfolio Performance

While we illustrate performance using four of our model portfolios, the 5-Year performance figures set out below are only representative. In practice, every client's portfolio is individually constructed to reflect their circumstances, objectives and capacity for risk.

| Portfolio | Risk Profile | 3-Month Return | 12-Month Return | 5-Year Return |

|---|---|---|---|---|

| Portfolio (A) | 5 | 13.26% | 29.61% | 64.83% |

| Portfolio (B) | 4 | 9.88% | 24.77% | 57.08% |

| Portfolio (C) | 3 | 7.55% | 18.92% | 42.29% |

| Portfolio (D) | 2 | 5.09% | 11.96% | 27.71% |

* Figures correct as at close of business 25/06/2026

The long-term results are clear: short-term volatility does not erase long-term compounding. Even with energy shocks, geopolitical crises, inflation scares and shifting central bank guidance, well-diversified portfolios continue to produce strong multi-year returns.

Looking ahead

The second half of 2026 is unlikely to be free from uncertainty. Inflation remains above central bank targets, geopolitical tensions have not disappeared entirely, and political developments in both the UK and US will continue to shape investor sentiment. But at Edgewater, our investment philosophy remains unchanged. Rather than attempting to predict short-term market movements, we continue to focus on building diversified portfolios designed to weather periods of uncertainty while participating in long-term global growth.

We believe successful investing is not about reacting to the latest headline. It is about having the discipline to remain focused on the journey, not the noise.

If you have any questions, concerns, or would like to discuss how these themes may affect your investment portfolio, please don't hesitate to contact us. We would be very happy to help you navigate the opportunities and risks ahead.

Market Insights

Our Investment Committee regularly publishes market updates, financial commentary, insights on Government policy changes and relevant policy developments that we believe you will find useful. These can be found on Edgewater's website (under "Insights"), as well as Edgewater LinkedIn and Edgewater Facebook pages. Please be sure to like and follow our channels to ensure you don't miss out on any new publications.

This article reflects our own interpretation and expectations regarding global macroeconomic and geopolitical developments. It is intended solely for general information and discussion purposes and should not be regarded as financial, legal, or professional advice.